Finding the Missing Millions

A handbook for using extractive companies’ revenue disclosures to hold governments and industry to account

Introduction

Oil, gas and mining companies based in Europe and Canada are now publicly disclosing the payments that they make to governments, including taxes, royalties and licence fees.

Companies are required to report payments in every country where they operate, and to report the payments separately for each individual project. The Extractive Industries Transparency Initiative (EITI)1 also now requires all implementing countries to report payments separately for each project.

These payments amount to hundreds of billions of dollars a year and are a vital source of government revenue, particularly in poorer countries. With project-level payment data in the public domain, governments can be called on to account for the receipt of these payments.2

But people in resource-rich countries also want to know whether companies are paying the correct amount of tax, and whether these payments represent a fair share of the natural resource wealth. These are not simple questions, but the disclosure of project-level payment data provides new opportunities to answer them.

Box 1: Where to find Payments to Governments reports

Canadian company reports are on a centralised site.

For European companies, use one or more of the following methods:

– Check resourceprojects.org.

– Do an Internet search, using the name of the company and “payments to governments” in quotations.

– Check the company website for financial reports.

– Payments to Governments reports may be included in the company’s annual report, or published as a separate, stand-alone document.

– Some companies that are registered in the UK report through the Companies House Extractives Service.

For EITI implementing countries, reports are available through the EITI Secretariat website.

This Handbook is designed to help you analyse payment data and identify potential losses in government revenue.

Where potential losses (or “red flags”) are identified, it is important to recognise that this is just the start of the process. Further inquiry will be needed. Care should be taken to ensure that convincing evidence supports any claims of revenue loss.

This Handbook is written in the hope that Payments to Governments data will be carefully analysed and that your findings will be both reliable and influential.

The Handbook is built around a set of 10 tests. Each of the tests assesses payment data in relation to other sources of information. The Handbook identifies the additional information that is required and where you might be able to find it.

The tests are organised from the simplest to the most complex. The early tests require little additional information and can be run by anyone with a few hours to spare.

The final tests require more detailed project-level data and a higher level of expertise.

The large volume of payment data being disclosed creates a challenge. Clear methodologies for using the data, like those provided in this Handbook, can help.

The methods set out in this Handbook are in the early stages of development and testing. By using them to analyse the growing body of payment data, we hope that they will be revised, refined and even replaced in the process of bringing greater accountability to the generation and collection of extractive industry revenues.

Box 2: Which companies report Payments to Governments?

If an oil, gas or mining company is listed on a stock exchange in the EU, UK, Norway or Canada, it is required to report payments to governments.

In Europe, transparency rules do not apply to companies that are listed on “non-regulated” stock markets, such as the UK Alternative Investment Market (AIM).

Private oil, gas and mining companies that are registered in the EU, UK, Norway or Canada are required to report payments to governments if they qualify as “large” companies.3

If you have difficulty finding out if a company is required to disclose payments to governments, one way to find out is to check if it has published a PtG report (see Box 1: Finding Payments to Governments reports).

Most oil, gas and mining companies that operate in EITI countries disclose their payments to governments in EITI reports. A list of countries that are implementing the EITI is here.

In some EITI reports, payments are disclosed at the company level. This means that if a company owns more than one project in an EITI country, the payment data from each project may be lumped together, making analysis of individual projects more difficult.

However, if a company only has one project in an EITI country, then the payments disclosed will be project level, making analysis of individual projects much easier.

How governments lose revenues

There are three main reasons why governments do not receive a fair share of extractive sector revenues: (1) the government struck a bad deal; (2) the company is employing aggressive tax avoidance strategies: or (3) government officials are not enforcing the rules. Sometimes it is all three.

Bad deals can be the result of government corruption, but they can also be the result of inexperience on the part of government negotiators, or the result of a conscious decision to offer investment incentives to extractive companies. It is often difficult to renegotiate bad deals even when the terms have been exposed. At the very least, public pressure can ensure that the same mistakes are not made again in future negotiations.

In circumstances where a government secures a good deal, revenues are often lost due to company tax avoidance practices. Companies can reduce their tax payments either by under-reporting project revenues or by over-reporting project costs.

The methodologies set out in this Handbook cannot provide definitive answers as to whether a government is securing a fair share of natural resource wealth, or whether there has been misconduct by any party. What they can do is identify discrepancies or “red flags”. In this report, a red flag is defined as a discrepancy between an expected payment and an actual payment.

Red flags are not by themselves an indication that companies are not paying what they owe. They should not be used, on their own, as the basis for public allegations of company wrongdoing. Where red flags are identified, it is important to recognize that this is just the start of the process.

In some cases, further analysis will identify reasonable explanations for the discrepancy. In other cases, unexplained discrepancies should be pursued using an appropriate combination of options, such as those set out in Box 3.

In all cases, care should be taken to ensure that convincing evidence supports claims of revenue loss.

Box 3: What to do if you identify a red flag?

If your analysis identifies a red flag, this does not necessarily entail wrongdoing on the part of the company or government. Further investigation will be needed to gather more evidence to support any claims of revenue loss. This could include:

– Carrying out further desk research into the discrepancy.

– Sending an email or letter to the company and/or the relevant government agency, highlighting your findings and requesting an explanation.

– If the country is implementing the EITI, raising the issue with the EITI Multi-Stakeholder Group.

If further investigation does not provide a satisfactory explanation, you may want to consider:

– Asking a politician to raise questions about the issue, for example in parliament.

– Lobbying official oversight bodies, such as tax authorities or anti-corruption agencies, to investigate.

– Contacting journalists to encourage media coverage.

– Raising the issue with relevant community leaders and working with them to secure accountability.

– If the company is publicly listed, encouraging investors in the company to raise questions with its management.

– Advocating for policy change, such as amending the fiscal regime for oil, gas or mining, if your analysis shows that a change is desirable.4

Analysing payments to governments

This Handbook highlights 10 individual tests that can be applied to Payments to Governments (PtG) data. Although the tests are different, the underlying methodology is the same.

In each case, the test focuses on the relationship between PtG data and other sources of data or information. The 10 tests are listed below, along with the additional information that would need to be collected for each.

The tests will help you determine whether a payment should have been made, and – importantly – how much you might expect a company to have paid. For example:

-

We might expect that the payments disclosed by a company would match government receipts.

-

We might expect a project that is producing commodities to be contributing at least some government revenues, such as royalties, from the start of production.

-

We might expect that a mature project should be paying profit-based taxes such as corporate income tax or production entitlements.

Each test follows a common series of steps:

1. Generate an expectation of what you think you should find.

2. Collect the secondary sources of data.

3. Perform the test.

4. Identify discrepancies (“red flags”) between the expected payment and reported payment.

Payments to Governments data

The table below sets out the main payments that companies disclose under payment transparency rules.5 It indicates when in the lifecycle of a project the payments are normally made (see Phase in the Project Lifecycle below). The table also identifies what specifically is being taxed.

Evaluating Payments to Governments data

Before analysing Payments to Governments (PtG) data it is important to be clear on what exactly is being reported. Here are some key issues that should be reviewed.

Reporting year

Is the company’s payment data based on a calendar year, or on some other reporting cycle (for example, July to June)? The company’s PtG report should state what the reporting cycle is.

It is important to check that the reporting cycle for the company’s payment data matches the reporting cycle for any additional sources of data you use in your analysis. This will ensure you are comparing like with like. For example, government data on commodity prices may be from a calendar year that is different from the reporting year used by a company in its PtG report.

Also keep in mind that company data may not be consistent either. For example, the company could report production that occurs at the end of one reporting year, while the sale of that production might be reported only in the following reporting year.

Reporting currency

Are the payments disclosed in a company’s PtG report in US dollars or some other currency? If you are using an additional source of data that uses a different currency from the PtG report, you will need to convert one or the other so that you are comparing like with like.

In these cases, check the company’s PtG report for the exchange rate being used. If the actual exchange rate is not reported, it will affect the reliability of your analysis. Alternatives include exchange rates provided by the Central Bank or various online tools such as Oanda or XE.com.6

Project partners

Is the project owned and operated by a single company, or are there other partners in the project, including other private companies or state-owned enterprises?

For projects where more than one company is involved, you will need to check whether the payments disclosed by a company in a PtG report relate to the project as a whole, or only to that company’s portion of the payment.

For example, sometimes companies make payments to governments on behalf of other companies in the same project, and report the whole amount in their PtG report. In these cases, the payment relates to the whole project.

In other cases, companies report only a percentage – their share – of a payment from a project.

PtG reports often include a section that explains which payments relate to the project as a whole, and which are reported as the company’s portion of a payment (see the “Basis for Preparation” section in PtG reports).

Helpful information on project ownership can also be found by doing a Google search on the project you are analysing, for example from a government source, a company website or in the industry press.

Information published by other companies involved in the same project can also provide a valuable source of additional information for the project you are analysing.

Project-level vs company-level payments

Sometimes companies operate multiple projects in a single country. Although companies are required to disclose payments separately for each individual project, payments such as corporate income tax may cover multiple projects. In these cases, the payments will be lumped together and reported at the company level (also known as “entity level”).

The company’s PtG report should make it clear which payments are project level, and which are entity level.

Supplementary data

To analyse the data in PtG reports, you will need to use additional sources of data.

Official government sources and formal company reporting to investors provide the most reliable data and are always preferable. For example, in countries that are implementing the EITI, EITI reports are often a good source of supplementary data. Government agencies often publish useful data on their websites, in some cases at the project level.7

For companies listed on stock exchanges, a reliable source will be their formal reporting to investors, found in annual reports, investor presentations or technical reports.8 These may be available on the company’s website, on the website of the relevant stock exchange (such as SEDAR in Canada, or EDGAR in the US), or through search aggregators like Open Oil’s Aleph.9

Private companies may also publish annual reports or have useful information on their websites. Additionally, they may be required to file documents with useful information through national corporate registries such as Companies House in the UK, Kamer van Koophandel in the Netherlands, or the Registre de Commerce et des Sociétés in Luxembourg.10

In some cases, state-owned oil or mining companies provide good project-level data.11

Industry and media reports provide an alternative source when official data is not available.

Fiscal terms

The “fiscal terms” for a project are the legal provisions that determine the types of payments a company must make to a government, such as bonuses, royalties, corporate income tax or production entitlements. The fiscal terms also clarify the specific ways in which each of the payments is calculated, including allowable deductions.

Understanding the fiscal terms that apply to a particular project is essential for many of the tests presented in this Handbook. It is important to try to identify the fiscal terms that are specific to the project you are analysing.

In some countries, the fiscal terms applicable to petroleum and mining projects are contained in national legislation and regulations. As legislation and regulations are commonly in the public domain, these should be easy to consult.12

In many countries, however, the fiscal terms covering petroleum and mining projects are set out in project-specific contracts (sometimes called host government agreements).

In some cases, project-specific contracts are publicly accessible on government websites (i.e. Ministry or EITI).13 Many of these will also be available at resourcecontracts.org. Unfortunately, however, for many projects the contracts remain secret.

Where full contracts are not in the public domain, summaries of the main fiscal terms are sometimes available. Governments may provide an overview of project-specific fiscal terms in official documents (e.g. Ministry publications or EITI reports). Donors such as the International Monetary Fund (IMF) and the World Bank sometimes publish analyses that contain information on fiscal terms.14

Companies may disclose a summary of the project-specific fiscal terms in their corporate filings. For publicly listed companies, look first for technical or “competent person” reports, or for the company prospectus or initial public offering (IPO) when the company was first listed.

Investor presentations, available on company websites, may also contain information on the fiscal terms, but these are often incomplete.

For oil and gas, it is common for governments to publish model contracts that establish the broad framework of the agreement. These can be helpful in determining the kinds of fiscal instruments that should apply to a project, but the specific terms are usually open to negotiation and therefore left blank.

If more reliable sources are not available, it may be necessary to use summaries of countries’ oil or mining fiscal regimes published by global accounting firms.15 It is common, however, for project-specific terms to differ significantly from those contained in these overview documents.

Revenue data

Some of the tests in this Handbook are based on comparisons of payment data in PtG reports with other sources of payment data such as EITI reports, or other official government publications such as budget documents.

Payment data published in a company’s PtG report can be compared with other sources of revenue data for the same year. For example, company payments can be compared with government receipts to check that they match.

An obvious secondary source of revenue data is EITI reports. However, the timelines for EITI publication mean that the data in these reports can often be two or more years behind.

Other potential sources of revenue data include official government disclosures or voluntary company disclosures.16 Joint venture partners reporting on the same project can be an additional source of revenue data as well.

Finally, data from the most recent PtG reports can also be compared to revenue data from previous years in order to assess trends.

Production, sales and costs

The advanced tests in this Handbook require more detailed project-level data. For several of them, it is important to identify overall project revenue, or to be able to estimate it by multiplying the volume of production by the sale price of the commodity.

Tests related to the payment of profit-based taxes, such as corporate income tax, also require reasonable estimates of current and past project costs.

The availability of project-level data on production, sales and costs varies widely. In some cases, governments publish project-level information on production volumes and sale price in EITI reports or on Ministry websites.

This data may also be available from the company itself. The data is often best for smaller, publicly listed companies that operate only one or a small number of extractive sector projects.

The largest extractive companies usually publish aggregate data. However, sometimes they disclose useful project-level information, for example in annual reports or on their websites.

For publicly listed companies, the best source of data on production, sales and costs is normally found in the company’s corporate filings.17 Investor analyses and documents on company websites can also be sources of information.

Other companies that participate in the project you analyse (“joint venture partners”) can be valuable sources of project-level information. This includes state-owned companies that hold a stake in the project.

In some cases these companies will report for the project as a whole.

Other times, a project partner may report data in proportion with its equity share.

For example, if a company owns a 50% equity share of a project, it may report 50% of the project’s production volume. In these cases, the data can be extrapolated based on the company’s equity share.

Box 4: Analysing company financial reports

Company financial reports are a potential source of project-level data. However, the data available within may not be readily comparable, as taxes in most countries are paid based on “cash-flow accounting” whereas most companies’ financial reports are based on “accrual accounting”.

In cash-flow

accounting, events are recorded on the date when cash is exchanged. In accrual

accounting, the transaction is recognized when the sale is made or the expense

incurred, even if the cash transaction has not yet taken place. This difference

can result in significant discrepancies in reporting at the end of a fiscal

year.

Other important differences between tax

accounting and financial accounting also need to be taken into account. For

instance, tax liabilities reported in financial statements rarely equal taxes

actually paid, as they include future tax obligations (deferred taxes); capital

investments are often claimed (depreciated) at different rates for financial

reports than for tax assessment; and operational data such as project revenues

often include sources of income other than the sale of commodities (e.g.

interest earned).

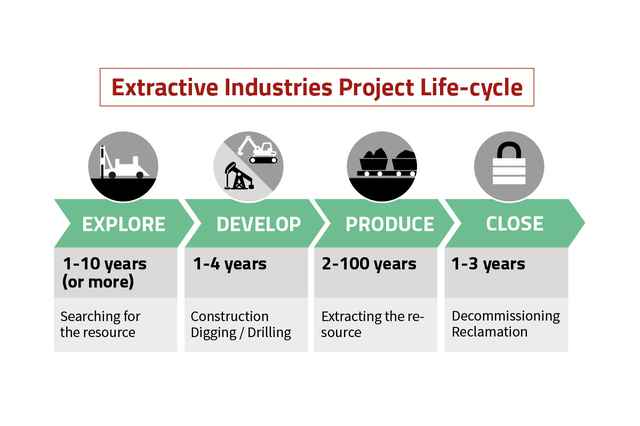

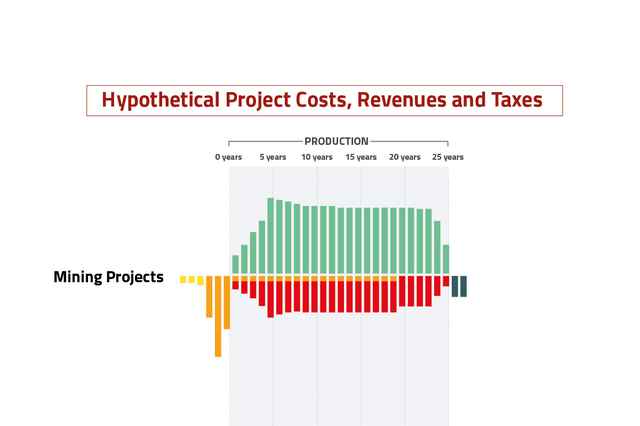

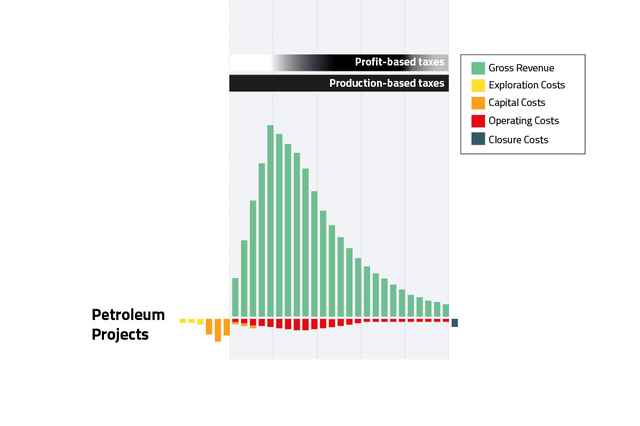

Phase in the project lifecycle

It is often important to identify the phase the project is at in the overall project lifecycle. This is because significant payments, including corporate income tax and production entitlements, may come on-stream only when the project has reached a mature phase of production. In contrast, other fees and taxes may apply throughout the project lifecycle.

Company websites or industry media reports are often a good guide for identifying the phase in the project lifecycle.

The company’s PtG report itself can also be a good indicator, as the inclusion of royalty payments or production entitlements means that the project is in the production phase.

Oil, gas and mining projects all follow a similar pattern, as described below.

The exploration phase involves the search for resources. Few payments to governments other than fees will be made at this stage, although potentially important signature bonuses or capital gains tax payments may also be made.

The development phase involves building the infrastructure to exploit the resource. As there is no production, there are likely to be relatively few payments to government at this point, other than fees.

The early production phase often involves a ramping up of the amount of resource produced. At this stage, companies will usually make payments based on production (e.g. royalties), but may not make any payments based on profits (e.g. corporate income tax, resource rent taxes), as they will be permitted to use the project’s profits to recover their upfront investment costs. This phase is often called the “cost recovery phase”.

However, in production-sharing systems, small profit-based production entitlement payments can be expected in the early production phase if there is a “cost recovery limit” in place (explained below in Test 7).

During the mature production phase the project is producing at high levels and initial investment costs have been recovered. This phase generates the bulk of government revenue. All of the main taxes should be generating significant revenue unless there has been a dramatic fall in commodity prices or significant new investment in the project.

The closure phase begins when the resource has been depleted or further extraction becomes non-economic.

Test 1: Checking that the right types of payments have been made

A simple but important test is to check that the company is making all of the types of payments that it should be.

It is best to start this test by identifying the fiscal terms that apply to the project. However, it is still possible to conduct the test if it is already clear to you that a payment should have been made.

For example, you may already know that a project is in production and should be paying royalties, or that a contract was signed and therefore a signature bonus was due.

Expectation

-

The company should report payments to governments for all types of payments that are applicable to the project.

-

All projects should report some kinds of payments, including surface taxes or annual licence fees, if they meet the relevant minimum threshold for disclosure.18

-

All producing projects should report production-based royalties, if royalties are based on either production volume or sale value.

-

Mature producing projects should normally report profit-based taxes.

Collect additional data

Performing the test

1. Check the company’s PtG report to identify which kinds of payments are being made.

2. Compare this with the types of payments that are applicable to the project.

Examples

1. Glencore in Chad

In its 2015 PtG report, Glencore reported paying zero royalties from its Mangara-Badila oil project in Chad. This appeared to be unusual as the project’s contract, which is in the public domain, shows that Glencore is required to pay a royalty based on a percentage of the sale value of the oil.19

It was clear that the project was producing oil in 2015, as Glencore’s PtG report showed that it paid production entitlements to the government. The company’s 2015 annual report also confirms that the project was in production.20

Action!

Global Witness wrote to Glencore to request an explanation. Glencore stated that the royalties were paid in 2015, but were aggregated with production entitlements in the PtG report. Glencore also stated that from 2016 onwards it would report royalties separately.21

2. Weatherly International in Namibia

In its 2015 PtG report, Weatherly International disclosed royalty payments for one of its copper mining projects in Namibia, but not for two other of its projects in Namibia that had been in production for some of 2015.22

Action!

The Natural Resource Governance Institute (NRGI) wrote to Weatherly to request an explanation. The company stated that because production had ceased for the latter two projects in 2015, it had overlooked more than $400,000 in royalty payments. Weatherly subsequently filed an amended PtG report including this information.23

3. African Petroleum in Sierra Leone

In its 2014 PtG report, African Petroleum disclosed an exploration licence fee payment of more than $900,000 in Sierra Leone.24 As licence fees are imposed from the start of the exploration phase and paid every year in Sierra Leone, one would expect a further payment to have been made in 2015. However, African Petroleum did not disclose a licence fee payment in its 2015 PtG report.25

Action!

Global Witness wrote to African Petroleum to request an explanation. At the time of writing, the company had not provided a response. Further steps would include contacting the relevant Ministry to ask whether the company contributed licence fees in 2015, and raising the issue with the EITI in Sierra Leone.

Plausible explanations

If a type of payment is missing, in the majority of cases this will not mean that the government is losing revenues. The reason for an expected payment being missing could be:

-

There was a reporting error.

-

The payment was made in advance during the previous year, or delayed until the next year.

-

There are project-specific tax exemptions, meaning no payment was required.

-

The project is recovering investment costs, or low prices made it unprofitable (if no profit-based taxes are reported).

It is possible, however, that the company is not making the payments that it should be.

Test 2: Tracking community-level payments

In many countries, the law requires a share of oil, gas or mining revenues to be returned to sub-national entities in the area where the extractive activity took place.

Sub-national entities can include affected communities, municipalities or provincial governments. Usually these payments are earmarked for spending on development projects to benefit local communities. Research by NRGI identified a (non-exhaustive) list of over 30 countries that have these local “revenue-sharing” mechanisms.26

Often the sub-national entity will be entitled to a percentage of royalty payments or a percentage of overall government revenue from the project.

This means that in many cases it is easy to identify how much a project should contribute to a sub-national entity, as it only requires a multiplication.

In PtG reports, companies are required to identify the government entity they make any payment to. This can enable you to track the money from company to community, and help ensure that it benefits affected communities.

In some cases, the company pays the central government, which is then responsible for transferring the funds to the sub-national entity. In other cases, the money is paid directly by the company to the sub-national entity itself.

In either case, PtG reports may help to identify the legally mandated amount of money sub-national entities should receive from a project.

Expectations

-

Payments to sub-national entities should equal the relevant payments reported by the company in its PtG report, multiplied by the relevant percentage.

Collect additional data

Perform the test

1. Calculate the expected sub-national payment by multiplying the relevant payments by the percentage to be allocated to the sub-national entity.

2. Contact the relevant government authorities to confirm the amount was paid and received.

Examples

1. Banro in the Democratic Republic of Congo

In the Democratic Republic of Congo (DRC), the mining law requires the central government to return a percentage of the royalties it collects back to the area where the mining activity took place.

Specifically, 25% of the royalties are to be paid to the province and 15% to the municipality or town where the mine is located. Research indicates that the central DRC government has not been transferring the full amount of royalties owed to its provinces.27

Banro Corporation operates the Twangiza gold mine in South Kivu province. In its 2016 PtG report, Banro disclosed royalty payments of C$1,280,000 from the Twangiza mine.28 A simple multiplication gives the amount in royalties that the Twangiza mine should have generated for the province and the municipality in 2016, to be transferred by the central government.

Action!

Global Witness wrote to Banro to request its comments on the Twangiza mine royalty transfers. The company had not responded at the time of writing. The next steps would be to contact the relevant central and sub-national authorities to confirm receipt of these payments, and to monitor their expenditure of the mining royalties to help ensure they benefit local communities.

2. Vedanta in India

In India, the district where a mine is located is legally entitled to receive 30% of royalties.29

Vedanta Resources operates the Codli iron ore project in the South Goa district. In its 2015 PtG report, Vedanta disclosed royalties of $7.1 million from the Codli mine.30

Multiplying this by 30% equals $2.13 million – the amount owed to the South Goa district from the Codli mine.

Action!

Global Witness wrote to Vedanta to request its comments on the Codli mine royalty transfers. The company had not responded at the time of writing. The next steps would be to contact the relevant sub-national entities to confirm receipt of the payment, and to monitor their expenditure of the mining royalties to help ensure they benefit local communities.

3. Nordgold in Burkina Faso

In countries where extractive companies are required to contribute a percentage of their turnover (or “gross revenue”) to sub-national entities, it may be possible to calculate the amount that companies should pay without using a PtG report.

Although the measure has not yet been implemented, Burkina Faso’s mining code requires mining companies to contribute 1% of their turnover to a Local Development Fund.31

In 2016, Nordgold reported gross revenues of $139.7 million from its Taparko gold mine in Namatenga province.32 In this case, the Local Development Fund is not operational, but if it were, Nordgold would have been required to contribute $1.39 million from the Taparko mine.

Test 3: Comparing payments and receipts

The original rationale for revenue transparency was to ensure that payments made to governments were actually received by the appropriate government entity and not diverted into private accounts. This test shows how mandatory reporting can contribute to this objective.

Simple comparisons between revenue data sources can uncover discrepancies and result in funds being recovered. This was the case with an $88 million discrepancy in the Democratic Republic of Congo.33

While more and more company payments are being disclosed under mandatory disclosure rules, in many cases the corresponding government receipts for these payments are not publicly disclosed. In these cases, you will need to request the data on receipts from the relevant government agency.

Expectations

-

Payments made by the company should match payments received by the government.

-

If two or more companies are reporting payments from the same project, the payment amounts should be proportionate to their respective equity stakes in the project. For example, if two companies report royalty payments from a project where they both hold a 50% stake, the royalty payments should be equal to one another. Some exceptions may exist, as addressed in ‘Plausible explanations’ below.

Collect additional data

Perform the test

1. Compare PtG data with government receipt data, or with PtG data reported by different companies within the same project, and note any significant discrepancies.

Examples

1. TOTAL in Angola

In its 2015 PtG report, the oil company TOTAL reported paying production entitlements to the Angolan government worth $1,535.2 million from Block 17.34 The Angolan government reported receiving production entitlements worth $3,729.6 million from Block 17.35

As TOTAL has a 40% share of Block 17, one would expect its payment to equal 40% of the government’s receipts.

However, calculations by a group of French NGOs showed that TOTAL’s payment did not equal 40% of the government’s stated figure. If this were the case, the total amount of production entitlements received by the government from Block 17 would have been $3,837.9 million, which is $108.4 million more than was reported by the government.36

In its response to the NGOs’ analysis, and in correspondence with Global Witness, TOTAL stated that it accounts for production entitlement volumes in accordance with the production-sharing contract, and values these volumes on the basis of regulated prices controlled and provided by the Angolan government, and that this excludes any possible manipulation of prices.37 TOTAL confirmed that it used the above-mentioned regulated price provided by the Angolan government in its 2015 PtG report, but declined to disclose the number of barrels that made up its production entitlement contribution from Block 17.

Action!

A next step in this test would be to further analyse the price assumptions underlying the two calculations.

2. TOTAL and Tullow in Uganda

Although Uganda is not yet an oil-producing country, international oil companies have made significant payments to the government. PtG reports are available for all three oil companies operating in Uganda: TOTAL, Tullow Oil and CNOOC Limited.

The Public Finance Management Act, passed in March 2015, created a Petroleum Fund designed to receive all oil-related revenues. The Act requires the relevant minister to table reports to parliament including “the source of the petroleum revenue”.

While the government had not yet reported to parliament at the time of writing, the Bank of Uganda does disclose some oil revenue receipts.

Unfortunately, the fiscal year used by the Bank of Uganda for reporting differs from that of the companies. Recognizing this limitation, the table below compares Bank of Uganda disclosures alongside 2015 payment data disclosed by Tullow and TOTAL.

The table shows that the government did not report approximately $14 million in payments disclosed by Tullow and TOTAL. This may have been because the payments were transferred by the Ugandan government into its temporary oil revenue holding account, which the government did not disclose receipts for. Tullow suggested that it may be because the Ugandan government does not consider some of the payment types shown in the table to be oil revenues (VAT, withholding taxes, national insurance, etc).

Action!

Equipped with this reconciliation information, Ugandan civil society representatives have had more valuable, in-depth debates with government officials to demand an explanation for the discrepancy.38 This included raising the issue in parliament as part of a presentation to the Public Accounts Committee.

3. Joint venture reporting in Nigeria

As stated above, when more than one company reports payments from the same project, the payment amounts can be compared to check that they are in proportion with each other. If a company seems to have paid less than expected, this may warrant further investigation.

Also, if there are other companies in a project that are not required to report payments, it may be possible to estimate how much they should have paid to the government.

Projects with more than one company involved are known as “joint ventures” and are very common in the oil, gas and mining industries.

NRGI analysed payment reports from joint venture partners in the Usan oil field (OML 138) in Nigeria.39 OML 138 is operated by TOTAL (20%), while other partners in the project include Chevron Corporation (30%), ExxonMobil (30%) and CNOOC Limited (20%).

TOTAL and CNOOC disclosed payments from OML 138 in their 2016 PtG reports.

Both hold a 20% stake in the project. We would therefore expect their payments to be the same.

CNOOC reports two separate categories of payments: royalties and taxes. TOTAL, however, reports only a tax payment and not royalties:

The combined royalty and tax payments from each company are nearly identical, suggesting that the discrepancies may be related to how the companies report.

Dialogue between NRGI and TOTAL confirmed that TOTAL aggregated royalty payments with taxes and reported both together in the tax category.

The other two joint venture partners – ExxonMobil and Chevron – were not required to report payments in 2016. However, we can project what their payments would have been based on the payment data reported by the other companies.

This can be useful for analysing payments by companies that are not required to disclose payments to governments, and for identifying the overall government revenue from a project.

Expected payments by each of the partners are based on the more detailed breakdown provided by CNOOC, and are set out in the table below (reported payments in bold, estimated payments in italics).

This analysis provides estimated payments for two American oil companies that are not required to disclose payments to government for OML 138 (Exxon and Chevron). It also suggests that revenues flowing to the Government of Nigeria from OML 138 from royalties and taxes should be around $130 million in total.

Action!

Next steps would be to check if the corresponding government receipts were published in an EITI report, and if so, whether they match the estimated payment figures. If no EITI data exists, you could request receipts from the relevant government agency. A further step could be to ask the companies that are not required to disclose payments if the estimated figures are correct.

Plausible explanations

Experiences within the EITI have demonstrated that there may be legitimate reasons why reported payments made by companies do not equal reported payments received by governments.40

Differing accounting methods used by companies and governments may account for discrepancies when comparing reported payments with reported receipts.

Data quality issues also need to be excluded before focusing on other explanations, such as the misdirection of funds, as data sources may simply be inaccurate.

When comparing payments made by joint venture partners, it’s also important to note that some payments should be proportionate to the company’s equity share, while others may not be. For example, royalty and production entitlement payments would normally be proportionate, while corporate income tax could be expected to diverge due to company-specific tax deductions.

Test 4: Confirming high-risk one-time payments

One-time payments made by companies – such as signature bonuses and capital gains tax – are particularly vulnerable to illegitimate diversion. This is because they can be very large, sometimes in the hundreds of millions. Furthermore, they are normally not integrated into formal payment and budget processes.41

It is particularly important, therefore, to check that one-time payments were made and match the government’s receipt, and to check that the amount is correct or seems fair.

In some cases, a PtG report could be the first public indication that a payment has been made.

Expectations

-

One-time payments were actually transferred to the government and the reported payments were equal to government receipts.

-

If the amount to be paid (a signature or production bonus) was stipulated in the project-specific contract, the reported payment should match this amount.

-

For capital gains tax payments, the amount paid should match the realized gain multiplied by the relevant tax rate.

Collect additional data

Perform the test

1. Confirm the passing of a milestone, requiring that a payment be made.

2. Check the PtG report to ensure that a payment was made and the amount. Note that bonuses are reported separately while capital gains taxes are grouped within the general tax category.42

3. Reconcile the payment reported by the company with the payment received by the government.

A more advanced test would be to recalculate the capital gains tax assessment based on the tax rate contained in the contract or tax law, the declared sale price of the asset and the actual or estimated “capital gain”.

Examples

1. TOTAL in the Republic of Congo

In July 2015, the oil company TOTAL renewed three oil licences in the Republic of Congo.43 One would expect TOTAL to have paid a bonus upon signing the renewal. However, no signature bonuses were disclosed for the Republic of Congo in TOTAL’s 2015 PtG report.44

Action!

Global Witness wrote to TOTAL to request an explanation. The company clarified that although the licence renewals were signed with the government in 2015, no payment was made in 2015 because the deal had not been approved by parliament by the end of that year. TOTAL also noted that ultimately there was no approval for the licence renewal, and the licences were handed back to the government at the end of 2016.

2. Shell and Statoil in Myanmar

In 2015, Shell and Statoil signed deep-water exploration contracts with the Government of Myanmar.45 Myanmar’s 2014 model oil contract requires a bonus be paid within 30 days of signing a contract (the actual amount is negotiable).46 However, neither of the companies reported paying signature bonuses in Myanmar in their 2015 PtG reports.

A review of publicly available sources suggests that the terms contained in Myanmar’s model contract were amended to make the bonuses payable within 30 days of the start of the petroleum operations, rather than upon signing a contract.47

Action!

Global Witness wrote to both companies to request an explanation. Statoil stated that no signature bonus was reported in 2015, as the contract requires it to be paid only if Statoil enters the next exploration phase, when it would have to commit to drilling exploration wells. Statoil told Global Witness that this is expected to start in 2018, but if the company decides not to enter the next phase no signature bonus will be payable. Shell also stated that it did not report a signature bonus in Myanmar, as none was required in 2015.

3. Eni in Mozambique

In its 2015 voluntary PtG report, Eni disclosed a $400 million capital gains tax (CGT) payment to the Government of Mozambique. The company first publicised the anticipated payment in a press release in 2013. The payment was based on Eni’s $4.16 billion sale to China National Petroleum Corporation of a 20% stake in the Area 4 block in 2013.48

The $400 million payment equalled 9.5% of the asset’s value. This was far lower than the CGT rate of 32% that was included in a law passed by parliament in 2012. That measure, however, had not been signed into law by the president, who cited concerns about its constitutionality. The Center for Public Integrity raised questions about how the 9.5% rate was determined, and about a lack of transparency over the process for assessing CGT.49

Action!

Global Witness wrote to Eni to request an explanation. The company confirmed that the sale of its stake in the Area 4 block was subject to taxation according to Mozambican law. Eni stated that the law, at that time, established a capital gains tax rate of 32%, but also allowed for a reduction to the tax base of 70% for assets held for more than five years.

Plausible explanations

The issue could simply be a matter of timing, as there are clear indications of signature bonuses and capital gains payments being agreed outside of the year in which they were actually paid.

There is also a risk, however, that the payments are never made; that they are too low; or that they are diverted from government accounts.

Test 5: Comparing payment trends over time

Comparing payments over time can highlight unexplained changes from one period to the next. This test can be particularly valuable in conjunction with EITI data, where historic EITI data can be linked with more up-to-date PtG data.

Expectations

-

Payments to governments should be similar from one year to the next, unless there are significant changes in production volumes, commodity prices or capital investments.

-

Fees can be expected to remain fairly constant from year to year. Assuming production volumes remain similar, value-based royalties are likely to fluctuate with commodity prices.

-

Profit-based taxes, such as corporate income tax and production entitlements, are the most susceptible to major swings. Increases can be expected as the bulk of investment costs are recovered, and decreases can be expected when new investments are made in a project, or when commodity prices slump.

Collect additional data

Perform the test

1. Construct a table to hold annual data for each type of reported payment.

2. Populate the table with current year payment data and previous year payment data.

3. Analyse trends for each category of revenue payments. If there are significant deviations from one year to the next – such as a steep drop in corporate income tax or royalty payments – this may warrant further investigation to determine the reason.

Examples

1. Tullow in Ghana

Tullow Oil has operated the Jubilee field in Ghana since 2010. The table below includes PtG data from the Jubilee field published by Tullow from 2011 to 2015.50

Royalty payments show a significant rise over 2011 to 2014, as would be expected with project production starting lower and then ramping up. Payment trends for corporate income tax show no payments in the first two years of production. This would be expected when initial project investment costs offset project revenue. However, significant income tax payments made in 2013 and 2014 contrast sharply with no payments in 2015.

Action!

Further analysis by NRGI, shown in more detail in Test 9 below, indicates the zero corporate income tax contribution in 2015 resulted from falling oil prices and the effects of Tullow using capital investments made in neighbouring oil fields to offset income generated by the Jubilee field.51

In correspondence with Global Witness, Tullow stated that the decline in corporate income tax payments for 2015 was partly due to some changes in the timing of tax payments for the year. Tullow also stated that it is not in dispute with the Ghanaian government in respect of this matter.

2. Rio Tinto in Mongolia

Rio Tinto operates Oyu Tolgoi in Mongolia, one of the largest copper and gold mines in the world. The mine began producing in 2013. Payment data is available for three years: 2016 data comes from Rio Tinto’s voluntary tax payment report;52 2015 data comes from Rio Tinto’s mandatory PtG report;53 and 2014 data comes from Mongolia’s EITI report.54 The table below shows annual royalty payments as reported from these sources.

The drop in royalty payments in 2016 seems unusual. The fiscal terms for the project, which are in the public domain, impose a royalty that is based on the sale value of the commodities (5% for both copper and gold).55

A first step is to check whether lower production volumes or commodity prices were responsible for the drop in royalties in 2016. Copper production stayed constant in 2015 and 2016 and was somewhat higher compared with 2014. Gold production was down in 2016 but not enough to account for the large drop in royalty payments.56

Similarly, a modest decline in copper prices in 2016, combined with a modest increase in gold prices, would not fully explain the large drop in royalty payments.57

Action!

Global Witness wrote to Rio Tinto to request an explanation. Rio Tinto stated that the amounts paid in royalties in 2015 included payments from earlier years, while some royalties in respect of 2016 were actually paid in 2017. In addition, 2016 royalties were lower due to the lower copper price and lower gold production in 2016.

3. Nordgold in Burkina Faso

Nordgold operates the Bissa gold mine in Burkina Faso. Its revenue payment data is shown in the table below.58

According to Nordgold, the mine began production in 2013, which would explain the zero contributions in 2011 and 2012.59 Corporate income tax was not paid in the first year of production, but was paid in the subsequent two years.

Royalty payments, based on the sale value of the gold produced, were substantial in 2013 and 2014 but zero in 2015. This would be considered unusual since it appears that the mine was still in production.

Action!

Global Witness wrote to Nordgold to request an explanation of the discrepancy. At the time of writing, the company had not provided a response. Next steps could include contacting the relevant government agencies to request an explanation, and raising the issue with Burkina Faso’s EITI.

Plausible explanations

Trend analysis can be expected to reveal significant changes in payments over time. The challenge is to find the underlying cause or causes. Fluctuations in commodity prices are likely to affect all of the main sources of government revenue, including royalties, taxes and production entitlements (see Test 8).

Trend analysis should reveal a growth in profit-based taxes as a project transitions from early year production, where investment costs are being recovered, to mature production (see Test 9).

Test 6: Verifying value-based royalty payments

Royalties are often the easiest of the main sources of government revenue to analyse. This is because in many countries the amount in royalties paid by a company is simply a percentage of the value of the commodity produced and sold from a project. These are known as “value-based” or “ad valorem” royalties.

If the value of the commodity produced and sold from the project is reported or can be calculated, it is possible to check whether the value-based royalty payments disclosed by companies seem correct.

In some cases, royalty payment analysis can also help to uncover the project’s royalty rate where the contract terms are confidential.

It is important to note, however, that there are other ways in which royalties can be calculated. Sometimes, costs such as transportation and processing are deducted before the royalty is assessed. Sometimes royalties operate on a sliding scale based on production volumes or commodity prices. It is important, therefore, to try to obtain the fiscal terms, which will include this information.

Other times, royalties are based on the profits made by companies. If this is the case, the royalty payments should be analysed using methods similar to those used for corporate income tax (see Test 9).

Expectations

-

When based on commodity value, royalty payments disclosed in PtG reports are approximately equal to the project-specific royalty rate multiplied by the sale value of the commodity (production x price). For example, if a company produces 10 million barrels of oil from a project, sells it for $50 per barrel, and the royalty rate is 5%, you would expect the company to pay $25 million in royalties.

-

Where the royalty rate is confidential, the royalty payment disclosed in PtG reports, analysed in conjunction with gross project revenue, can reveal the actual royalty rate. For example, if a company produces 10 million barrels of oil from a project and pays $25 million in royalties, you would expect the royalty rate to be 5%.

Collect additional data

Perform the test

1. Check that the royalty regime is based on the sale value of production.

2. Identify the relevant royalty rate and, if possible, whether there are any allowable deductions such as transportation or processing.

3. Calculate the expected royalty payment by multiplying the value of the project’s production (gross project revenue) by the royalty rate.

4. Compare the results with the royalty payment as stated in the company’s PtG report.

Examples

1. Avocet in Burkina Faso

Mining royalties in Burkina Faso are based on the sales value of production. Royalty rates for gold vary according to the gold price: 3% up to $1,000 per ounce; 4% between $1,000 and $1,299 per ounce; and 5% from $1,300 per ounce.60

Avocet Mining operates the Inata gold mining project in Burkina Faso. In its 2015 annual report, Avocet stated that the value of its gold sales in Burkina Faso was $85,038,000.61 As the Inata mine was Avocet’s only producing asset in 2015, we can assume that all of its gold production came from there.

The gold price did not fall below $1,050 per ounce in 2015, suggesting that the applicable royalty rate should have been 4%. Multiplying $85,038,000 by 4% gives an expected royalty payment of $3,401,000.

However, in its 2015 PtG report, Avocet reported paying significantly less than this from the Inata mine: only $2,094,000.62

Action!

Global Witness wrote to Avocet to request an explanation. Avocet stated that as of December 2015 it had paid $2,094,000 in royalties, and that the remaining $1,307,000 was recorded as a liability and was paid in 2016.

2. Shell in Nigeria

Oil royalties in Nigeria are based on the sale value of production.

For oil extracted offshore at a water depth of 800 to 1,000 metres, the royalty rate is 4%. For oil extracted at water depths over 1,000 metres, the rate is 0%.63

Shell operates Oil Mining Licence 118 (OML 118) in Nigeria. The water depth of OML 118 ranges from 900 to 1,150 metres, putting it on the border of either a 4% or 0% royalty.64

In its 2015 PtG report, Shell disclosed an in-kind royalty payment from OML 118 of 703,000 barrels, worth $37,424,320.65 The Nigerian National Petroleum Corporation reported oil production for OML 118 at 70,030,598 barrels in 2015.66

As Shell is paying significant royalties, clearly it is not subject to the 0% rate. One might therefore expect the 4% rate to be in effect.

However, Shell’s in-kind royalty payment of 703,000 barrels from a production total of 70,030,598 barrels gives a royalty rate of 1% – far lower than 4%.

The explanation appears to be that a special royalty rate was being applied to OML 118. Nigeria’s 2013 EITI report indicates there is a dispute between Shell, which claims that a 1% royalty applies to OML 118, and the Nigerian government, which claims that the royalty should be 1.75%.67

Action!

Global Witness wrote to Shell to ask what the royalty rate was for OML 118 in 2015, and whether the company is in dispute with the Nigerian government over the royalty rate. Shell stated that it adheres to the disclosure requirements of the UK’s Payments to Governments Regulations, which do not require companies to disclose contract terms.

3. Monument Mining in Malaysia

Mining royalties in Malaysia are generally based on the sales value of production. According to a technical report published by Monument Mining, the royalty rate applied to its Selinsing gold mine in Pahang State is 5%.68

Using project-level production and price data disclosed in Monument’s 2016 annual report, Publish What You Pay Canada (PWYP-Canada) analysed the Selinsing mine’s royalty contributions for 2016.

Because Monument reported details of a forward sales contract in place in 2016, PWYP-Canada added two different figures to calculate the expected amount in royalty payment.

The figures in Monument’s annual report that were used to calculate the expected royalty payment are in US dollars, but in its 2016 PtG report, Monument disclosed a royalty contribution from the Selinsing mine in Canadian dollars, of C$1,510,000.

This means we need to convert our expected royalty figure of $1,179,725 into Canadian dollars. This comes to C$1,557,237 – a close match to the C$1,510,000 reported by Monument. The relatively small discrepancy is likely to come from the currency conversion.

4. Nostrum in Kazakhstan

Nostrum produces oil and gas from its Chinarevskoye project in Kazakhstan. The main fiscal terms contained in the production sharing contract were disclosed by the company in a prospectus published in 2014.69

The terms include a royalty payment for both oil and gas that increases based on the volume of production, as set out in the table below. The prospectus also clarifies that the royalty is calculated on sales “less the cost of transportation to its final destination”.70

In its 2015 annual report, Nostrum discloses production volumes and revenues for both oil (16,877) and gas (23,514) in barrels of oil equivalent per day (boepd).71

In order to apply the royalty rates in the table above to Nostrum’s production, the oil production needs to be converted from boepd to tonnes (840,396), and the gas production figures in boepd need to be converted to 1,000 m3 (1,287,392).72

After converting the units of production, we apply the royalty rates as set out in the table above to Nostrum’s reported production volumes. The result is a 4.8% average royalty rate for oil and a 4.1% average royalty rate for gas.

As the royalty payment to government includes both oil and gas, we need to combine the average oil royalty of 4.8% and the average gas royalty of 4.1% into a composite royalty. To do this, we need to return to analysing volumes in millions of barrels of oil equivalent (mmboe). As shown in the table below, the estimated composite royalty is 4.4%.

Nostrum’s PtG report confirms that its royalty payment was paid in cash and not in kind. As a result, the royalty test can be calculated in dollars rather than volumes of oil and gas. Nostrum reports overall revenue at $448.9 million.73 The company also reports transportation costs of just over $45 million.74 According to the fiscal terms, transportation costs are deducted before the royalty is assessed.

Our expected royalty payment, therefore, is 4.4% of $403.8 million, which equals $17.8 million, as shown in the table below.

In its PtG report, Nostrum reports a royalty payment to the Government of Kazakhstan of $17,142,173.75 The difference between the expected payment and the actual payment is around $600,000.

Action!

As the estimated royalty is somewhat higher than the reported royalty, a further step would be to determine whether there were other deductions, in addition to transportation costs, that should be subtracted before calculating the estimated royalty payment.

Plausible explanations

In many cases, there will be significant discrepancies between the expected royalty payment and the royalty payment reported by a company. The discrepancies may be related to the quality of the data. For example:

-

Production may be sold within a particular year, but delays can mean the royalty payment is not made until the following year.

-

Some costs (e.g. transportation, processing) may be deducted before the royalty is assessed.

-

The value of a commodity used in the calculation of the royalty may differ from the value reported in the PtG reports for in-kind contributions or in other company-based reporting.

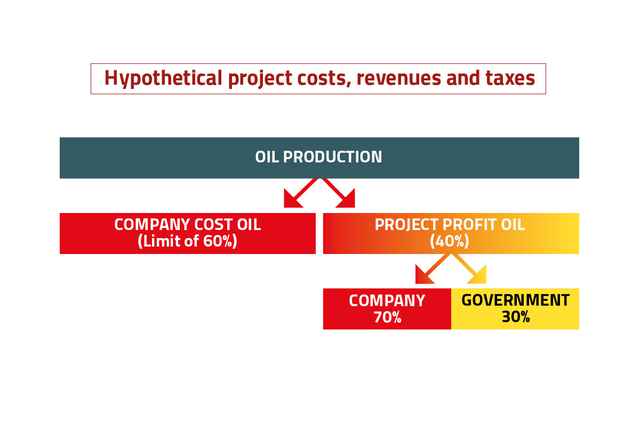

Test 7: Verifying early year production entitlements

Production entitlements are payments made to governments from oil and gas projects governed by production sharing contracts or agreements. In production sharing systems, governments and companies divide the volume of production that remains after costs have been recovered.

The production that remains after costs have been deducted is normally called “profit oil” or “profit gas”. In PtG reports, profit oil is normally referred to as a “production entitlement”. It will commonly be the single largest source of government revenue over the lifecycle of the project.

While the underlying logic of production sharing systems is relatively simple, analysis of production entitlements requires access to detailed contract terms, particularly on the allocation of profit oil.

As production entitlements are assessed after costs, it is normally necessary to conduct detailed analyses of both current year and past year costs (see Tests 9 and 10 below).

However, when a project is in the early years of production, it may be possible to perform a test on production entitlements that is similar to the test on royalties, as described in Test 6.

This is because many production sharing contracts often include a limit on the amount of production that the company can allocate in any one year to recover its costs. This provision is commonly referred to as a “cost recovery limit” or “cost recovery cap”.

In the early years of a project, accumulated costs will almost certainly exceed the limit allowed for cost recovery. In these circumstances, the amount of profit oil remaining after costs have been taken into account can be determined simply by knowing the cost recovery limit as set out in the contract.

For example, assume a production sharing contract has a cost recovery limit of 60% and the remaining production (the profit oil) is shared 70% to the company and 30% to the government.

Assume, also, that allowable cost claims exceed the cost recovery limit.

If the project produces $1 billion of oil, we know that $600 million would go to the company as cost oil.

The remaining $400 million profit oil would be divided between the company and the government – $280 million to the company and a $120 million production entitlement payment to the government.

Expectations

-

The volume or value of the government’s production entitlement in the early stages of a petroleum project should equal the minimum allocation allowable under the terms of the production sharing contract.

Collect additional information

Perform the test

1. Identify the cost recovery limit and the percentages of production allocated to the government and to the company once costs have been recovered.

2. Identify (or calculate) the gross project revenue (volume of production multiplied by sale price).

3. Calculate the value of the minimum share of production that should flow to the government (including the royalty if relevant).

4. Compare your calculated figure with the production entitlement payment, as disclosed in the company’s PtG report.

Examples

1. Glencore in Chad

Glencore’s Mangara-Badila oil project in Chad began producing in 2013/2014. The contract is public.76 There is a 14.25% royalty assessed on overall production. From the remaining production, up to 70% can be allocated to cost recovery. In the early stages of the project, 40% of the remaining production (profit oil) is allocated to the government.77

In its 2015 annual report, Glencore stated that gross production from its oil assets in Chad was nearly 7.7 million barrels.78 As the Mangara-Badila project appears to be Glencore’s only producing oil asset in Chad, the 7.7 million barrels can be attributed to this project.

The sale price of the oil was unclear, as Glencore reported only the average price of Brent Crude at $54 per barrel.79 Starting from Brent Crude, it is possible to estimate the oil price by taking into account a deduction estimated at 5% for lower quality oil and the cost for using the export pipeline of $8 per barrel.80 The estimated sale price therefore would be around $43 per barrel.81

Multiplying production by the estimated $43 per barrel results in a gross project revenue of just over $331 million.

The first step in calculating the expected payment to the government is deducting the 14.25% royalty estimated at just over $47 million ($331,057,000 x 0.1425).

Cost and profit oil calculations can then be made based on the remaining production.

As the project is in its early stages of production, we can assume that the full allowable 70% will be allocated to costs. The contract states that of the remaining 30% allocated to profit oil, 40% would go to the government, which represents a net 12% after the royalty payment.

According to the calculations below, the expected production entitlement payment would be around $34 million. Based on the assumptions set out above, we would expect the royalty payment and production entitlement to amount to just over $81 million.

In its PtG report, Glencore reports no royalty payment and a production entitlement payment of just over $73 million. We assumed that Glencore reported the royalty and production entitlement payments together. The difference between the combined expected payment and the combined reported payment is around $8 million. We presume that the difference was likely the result of a difference in the sale price used for the fiscal calculations.

Action!

Global Witness wrote to Glencore to seek clarification. First, Glencore acknowledged that they reported the royalty and production entitlement payments together as one lump sum. Second, Glencore pointed out that there was a small difference between the publicly reported volume produced and the actual volume sold, with sales being 41,000 barrels lower. Third, Glencore confirmed that our estimated sale price was too high and that the actual sale price was around $40/bbl, and that the market discount for the grade of oil was higher than estimated by Global Witness.

Finally, Glencore stated that it does not include transportation tariffs, which are agreed directly between the pipeline operators and the government of Chad and to which it is not privy. Making adjustments on the basis of Glencore’s statements reduces the payment by $7.9m. This broadly reconciles our estimate with the amount declared by Glencore.

2. Wentworth in Tanzania

Wentworth Resources is a partner in the Mnazi Bay natural gas project in Tanzania, along with Maurel & Prom and the Tanzania Petroleum Development Corporation (TPDC), the Tanzanian national oil company.

Although the production sharing contract for the Mnazi project has not been disclosed, the fiscal terms are available in a technical report published by Wentworth.83

Wentworth’s technical report indicates that there is a cost recovery limit set at 60%.

Profit petroleum is then allocated on a sliding scale based on the volume of gas produced according to the following table. As the volume of gas produced increases, the government share also increases.

Wentworth’s 2016 annual report states that the Mnazi project was still in the cost recovery phase, meaning that we should expect a full 60% of production to be allocated to costs, leaving 40% of production for profit petroleum to be shared between the company and the government.

Wentworth’s latest annual report includes the average daily volume of gas produced for the whole project in 2016. After converting this into an annual production figure, it is possible to estimate the volume of both cost and profit gas.

The allocation of profit gas depends on the volume of gas produced as set out in the “profit gas allocation” table above.

Note that for the volume of gas produced by the project, all four of the profit-sharing tranches are engaged. The first tranche of 2.5 mmscf is split 50:50, the next tranche of 2.5 mmscf is split 60:40, the next tranche of 5 mmscf is split 35:65, and so on.

The calculation is set out in the table below.

In Wentworth’s 2016 PtG report, they indicate: “As the Company’s operations in the country consist of a single project the amounts reported in the consolidated overview represent all payments by project during year”.84 We assume, therefore, that the reported production entitlement includes not only profit gas allocated to the government, but also the cost gas and profit gas allocated to TPDC based on its 20% stake in the project. The table below shows our expected production entitlement from these three allocations.

According to the calculations above, we would expect a production entitlement of 6,556 mmscf. In its 2016 PtG report, Wentworth indicates that the actual host government entitlement was almost exactly the same: 6,565 mmscf.

Plausible explanations

The logic of this test is similar to a royalty test. However, there are more calculations involved and therefore a greater likelihood of divergences between reported and estimated payments.

Data on production volume may be available. Some divergence should be expected if converting from daily averages to annual total production.

If the test is run based on the value of production rather than volume, as was the case for Glencore above, some divergence may be due to assumptions related to sale value. Many companies reporting payments “in kind” use an average price that may not be project specific. If the reported production entitlement is greater than the calculated production entitlement, it may be that the bulk of past costs have been recovered and that the cost recovery limit is no longer being reached.

Test 8: Assessing fair market commodity value

It is important to check that the sale price of a commodity used for the calculation of royalties and taxes is in line with the international market value of the commodity. This is because under-reporting the true value of a commodity can be a major source of government revenue loss.85

If a commodity is sold to an affiliated company, there is a risk that under-reporting the true value can result in the shifting of profits out of the producing country.

In some cases, these transactions are based on long-term sales contracts. The terms of these sales contracts can be entirely appropriate, and can generate additional government revenue when international market prices fall. However, they can also lock in an artificially low sale price.

As all major government revenue streams are based on the declared sale price of the commodity, under-reporting would result in revenue loss for both royalties and profit-based taxes such as corporate income tax and production entitlements.

In some cases, the company will report the sale price of the commodity in public reports. If this is the case, it can be directly compared with an international market price.

In other cases, it may be possible to combine PtG reports and other public domain information to determine the sale price of the commodity used for tax calculations. This can then be compared against an international market price.

If there is a significant discrepancy, the reason for the difference should be investigated, particularly where the commodity is sold to an affiliated company.

Expectations

-

The sale price of the commodity used for fiscal calculations will be close to the price for that commodity, as reported in international markets, with differences accounted for by the quality of the commodity or eligible cost deductions such as transportation.

Collect additional data

Note that this test can be done in two different ways: (1) using the gross project revenue as reported by the company compared with reported production multiplied by an international benchmark price; or (2) comparing the effective sale price at the unit level (e.g. price per barrel of oil, price per ounce of gold) with the international benchmark price. The information needed is different depending on which approach you use.

Perform the test

1. Identify or calculate the commodity price used for fiscal calculations. Check if the company reports the sale price directly. If not, calculate the effective sale price by dividing project revenue by project production.

2. Compare the reported sale price with an international benchmark price.

3. If the reported gross revenue (or unit price) is significantly lower than the international benchmark price, carry out further investigation.

Examples

1. Shell in Nigeria

In Shell’s 2015 PtG report, its Nigerian subsidiary – Shell Petroleum Development Company (SPDC) – reported the volume and value of in-kind payments to the Nigerian government for five distinct projects.86

The projects produce both oil and natural gas. Shell combines the oil and gas elements of its in-kind payments and reports them as a “barrel of oil equivalent” (BOE).

Because Shell reports both the value and volume of production, the data allows us to calculate a BOE unit value figure for each project.

The results are given in the table below, and show that the BOE price for SPDC East was far lower than the rest of the projects, at $21.87

This analysis was constrained by the fact that the SPDC East ‘project’ is in fact made up of several separate projects that Shell lumped together for the purposes of reporting. The Nigerian government publishes data on oil and gas production at the project level. If Shell had also reported data at the project level, it would have been possible to use the government data to move the analysis forward.

Action!

Publish What You Pay UK wrote to Shell to request an explanation. The company clarified that the in-kind payment for its SPDC East project included a gas component as well as oil, hence the lower value. Shell stated that the oil component was valued at $53.50 per barrel, but declined to provide further details of the breakdown between oil and gas production.

Global Witness also wrote to Shell to request a breakdown of the oil and gas components. Shell stated that it adheres to the disclosure requirements for payments in kind, and that in addition, the company publishes production data for Nigeria on a quarterly basis in its “Supplementary Financial and Operational Disclosure” reports.88

Further analysis is needed to determine whether the $21 BOE figure represents a fair market price. A next step would be to determine production volumes of both oil and gas in order to determine the effective price of gas sales. Analysis could also focus on whether a gas sales agreement exists.

2. Glencore in Chad

In the Glencore example from Chad in Test 7 above, we generated an expected payment for both royalties and production entitlement based on:

-

The volume of oil production reported by Glencore.

-

The fiscal terms in the contract, which is in the public domain.

-

An estimated oil price based on Brent Crude, with deductions for quality and transportation based on corporate filings.89

The sale price of Glencore’s oil from Chad is controversial, not least because Glencore is both the seller and the buyer.90 Furthermore, there is limited information in the public domain on the price at which Chadian crude sells below the international benchmark (Brent Crude) or the costs of exporting the oil by pipeline.

The preliminary conclusions of the analysis in Test 7, and Glencore’s response, indicate that our estimated oil price might have been too high. By combining public domain information – including production volumes, tax terms and company payment data – it is possible to calculate the effective sale price.

The fiscal terms tell us the minimum share of production that should be allocated to the government: a royalty of 14.25%, in addition to 10.29% of production (see Test 7). The minimum government share of production would therefore be 24.54%.

If Glencore’s payment to Chad’s government of just over $73 million constitutes 24.54% of overall project revenue, then overall project revenue would be almost $299 million. If the project produced nearly 7.7 million barrels of oil and generated nearly $299 million in overall revenue, then we would expect an effective sale price of just under $39 per barrel.

Action!

Global Witness wrote to Glencore to seek clarification on the effective sale price. Glencore replied that the effective sale price was $40 per barrel.

A discrepancy of $1 per barrel remains between our expectation and Glencore’s reported sale price. To take this analysis forward, the next step would be to try to further clarify the difference between the discount for oil quality and the costs associated with pipeline transportation.

Plausible explanations